Turbulence in U.S. Treasury Markets - Q3 2023

The turbulence in treasury markets, throughout most of Q3 2023, has sent shockwaves through the global economy and the implications are far-reaching. US treasuries, which are one of the most important global markets, are experiencing a storm of uncertainty as treasury bonds undergo a repricing.

Yields on long-duration treasuries hit a 16-year high this week, marking a dramatic shift from the relatively stable environment of the last couple of decades. The recent spike in yields, driven by investors selling treasury bonds, reflects expectations of sustained high-interest rates. This anticipation was further fueled by unexpectedly strong economic data that propelled yields on 10-year treasuries to a staggering high of 4.88%.

What makes the situation more perplexing is the simultaneous turbulence in the stock market. Historically, stocks and bonds move in opposite directions, acting as a counterbalance in times of volatility. This year, both assets have been falling in tandem. With treasuries on track to post annual losses for a third straight year, a first in US history according to Bank of America, investors are increasingly grappling with new realities.

The confluence of factors—Federal Reserve policy decisions, mounting concerns over federal debt, and the forthcoming issuance of new treasury bonds—has given rise to a perfect storm. This article will explore the factors contributing to this bond selloff and what it means for the broader economic landscape.

Fed Policy

One driving force behind the recent surge in treasury yields can be attributed to the monetary policy decisions made by the Federal Reserve. Following rapid interest rate hikes by the Fed to quell rising inflation, the Fed policy rate now sits above 5%, a dramatic departure from a decade of near-zero interest rates.

While this rapid rise in interest rates has impacted shorter-duration treasuries, long-duration bonds have not reacted as drastically, due to expectations of near-term interest rate cuts. Now, after a hawkish Fed meeting and a stronger-than-expected job report, investors are fretting that the Fed will hold its policy rate higher for longer. This led to a selloff in long-duration treasuries that sent the yield on 10-year treasury bonds to 4.88%, the highest level in more than a decade in a half.

Adding to the complexity is the Feds current policy of Quantitative Tightening (QT) where the Fed reduces its balance sheet by allowing maturing bonds to roll off without reinvesting the proceeds. This stance removes the Fed as a significant buyer of treasuries, further contributing to upward pressure on yields as the bond sell-off continues.

Deficits and Debt Issuance

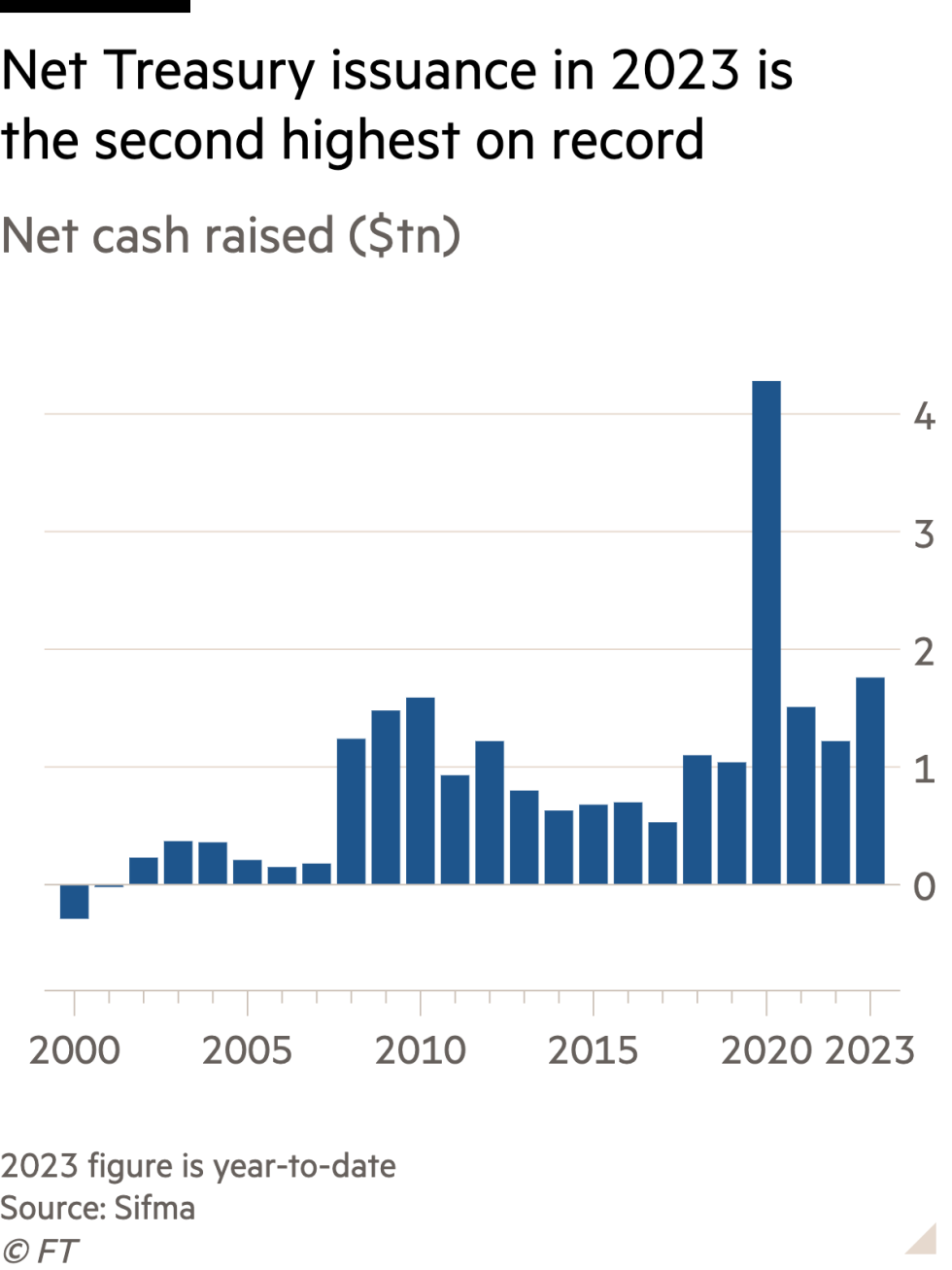

Following 22 straight years of US government deficits and a recent downgrade in US debt to AA+ by credit rating agency Fitch, the US Treasury announced further plans to borrow $1 trillion in the third quarter of 2023. In terms of net treasury issuance, 2023 is second only to the record-setting year of 2020 during the COVID-19 pandemic, which saw more than $4 trillion issued.

As the chart below shows, the net Treasury issuance in 2023 is the second highest on record.

With fresh treasuries hitting markets in the coming weeks, and a drop in demand for these bonds, the toughest challenge may yet be ahead of us. This surge in supply, paired with the Fed stepping away as a buyer of US treasuries, could depress bond prices and drive yields even higher.

Furthermore, fears of a US debt crisis, driven by the debt ceiling debacle earlier this year and ballooning interest payments on outstanding debt have further contributed to the sell-off. Investors are demanding a higher return for holding their money in bonds, which are beginning to seem less ‘risk-free’ than they have been made out to be. At the time of writing, US federal debt stands at $33.5 trillion, interest payments on outstanding debt near $1 trillion, and the debt-to-GDP ratio exceeds 123%.

What does this mean for the Economy?

If treasury yields continue their ascent, it will have negative implications for the economy. Rising borrowing costs will increase expenses for consumers seeking loans and mortgages. Gradually, the escalation in borrowing costs will exert additional pressure on an economy that has yet to adjust to the swift rise in the policy interest rate over the last 18 months. If yields push above 5% on the 10-year treasury, it makes the possibility of a recession even more likely.

Furthermore, high yields will spell bad news for risk assets. As the yield rises on treasuries, investors may rotate out of stock markets towards high-yielding treasuries which promise possible returns above 5% for holding ‘risk-free’ government bonds.While the path forward remains uncertain, the treasury market’s fluctuations, influenced by an interplay of factors, serve as a stark reminder of the intricacies of the global economy.

As yields continue their ascent, we find ourselves at a critical juncture where the decisions of policymakers, businesses, and individuals will ripple through the economy. Potential consequences are significant, casting a shadow over various facets of the economy. From escalated borrowing costs, which can strain consumers and deter investment, to looming negative impacts on risk assets, these repercussions should not be underestimated.

The broader economy may find itself at a crossroads, with the recent spike of treasury yields potentially impeding economic growth and even heightening the possibility of a recession. The interplay of Fed policies, mounting concerns about burgeoning debt, and an influx of new treasury bonds into the market underplays the complexity of the situation. As we navigate the path forward, adaptability and a keen understanding of the evolving economic landscape will be essential to weather the storm.