Bitcoin vs. CBDCs vs. Crypto

Theya is the world's simplest Bitcoin self-custody solution. With our modular multisig vault, you decide how to hold your keys.

Whether you want all your keys offline, shared custody with trusted contacts, or robust mobile vaults across multiple iPhones, it's Your Keys, Your Bitcoin.

Download Theya on the App Store.

The advent of Bitcoin set forth a frenzy of digital currencies. Today, over 22,000 cryptocurrencies exist as many have sought to capitalize on this digital currency boom. Historically, the current financial system and its incumbents have been resistant to innovation, but the advent of Bitcoin has ushered in an era of change, whether they embrace it or not. The risk of being replaced by superior technologies like Bitcoin has spurred central banks to develop their own technological solution: Central Bank Digital Currencies (CBDC). While CBDCs may be digital, they differ significantly from Bitcoin in terms of their operational mechanisms and inherent characteristics.

Many skeptics of Bitcoin falsely assume they can continue using the financial system as it is today. However, a wave of change has been thrust upon us. By dismissing Bitcoin, they are inadvertently choosing a CBDC. In fact, CBDCs are in the works at most central banks around the world today. Over 130 countries, representing 98% of global GDP are exploring a CBDC.

In this article, we will break down the key differences between Bitcoin and a CBDC so you, the reader, can have an informed opinion on whether opting into Bitcoin is a wise decision for your financial well-being.

What Is A CBDC In Simple Terms?

A Central Bank Digital Currency (CBDC) is a digital form of a country's official currency, programmable money, issued and regulated by its central bank. Unlike Bitcoin, CBDCs are typically centralized and backed by the government. CBDCs leverage blockchain or distributed ledger technology to enable digital transactions, potentially replacing physical cash and offering increasing traceability.

They could be used for a wide range of financial transactions for payment efficiency, while also serving as a tool for the central bank to implement monetary policies and monitor the economy to a greater degree than otherwise would be possible.

While promoted as a beneficial tool by central banks around the globe, there are justifiable concerns with the implantation of a central bank digital currency. Here are the two types of CBDCs to be aware of:

Retail CBDC Concerns

Retail CBDCs, designed for everyday use, grant governments unparalleled access and control over personal spending, raising censorship, surveillance, and privacy concerns. For example, China's CBDC pilot would amplify the already problematic social credit system, heightening worries about human rights.

Wholesale CBDC Concerns

Wholesale CBDCs focus on improving the efficiency and security of transactions between commercial banks and financial institutions rather than direct public use, promising to streamline interbank operations. However, this focus on the institutional level does not exempt them from criticism.

CBDCs centralize power further within central banks, enabling more direct control over monetary policy and financial stability mechanisms. This could perpetuate the "too big to fail" problem and moral hazard within the fiat banking system, where banks are incentivized to continue taking on greater risks knowing they have central bank support.

CBDCs vs. Crypto

CBDCs and cryptocurrencies are often conflated, yet they differ significantly. Although Central Bank Digital Currencies may utilize blockchain technology, they are fundamentally centralized and governed at the state level. They are the antithesis of Bitcoin, an open-source protocol offering financial self-sovereignty.

And it's important to note that while the "crypto" industry is rife with claims of decentralization, most projects are akin to tech company ventures rather than genuine forms of digital money.

"Bitcoin, not crypto" is a common adage for a reason. It's the only decentralized ledger (blockchain) that is secure without a centralized third-party.

CBDCs vs. Bitcoin

Bitcoin is a decentralized digital currency that operates on a peer-to-peer network, enabling direct value exchange without intermediaries. It has a finite supply of 21 million coins, making it deflationary and immune to monetary inflation.

Unlike a CBDC, Bitcoin is not controlled by any central authority, providing greater autonomy to its users. It is a borderless and pseudonymous form of money, offering more privacy in transactions and higher financial inclusion.

Additionally, its decentralized nature makes it resistant to government intervention or manipulation, which allows it to serve as a hedge against inflation and a way to preserve wealth.

Various CBDCs will exhibit operational differences depending on how their central bank implements them. Below, we'll explore the fundamental distinctions between Bitcoin and a CBDC based on our current understanding.

Supply Dynamics

Currently, the exact supply dynamics of a CBDC remain uncertain. CBDCs would have an infinite supply, assuming they mirror traditional fiat currencies, rendering them susceptible to inflation and devaluation over time.

In contrast, Bitcoin is limited to a finite supply of 21 million coins, making it naturally deflationary and immune to inflation.

When saving your money in a CBDC, you will lose purchasing power over time, whereas if you save in Bitcoin, you will gain purchasing power over time. This is the critical difference between an inflationary and a deflationary currency.

Centralized vs. Decentralized

CBDCs are inherently centralized. These digital sovereign currencies would be issued and regulated by national central banks, with each country implementing its own CBDC for use in its domestic economy. While CBDCs may be interoperable or used abroad for trade, decisions surrounding their fundamental operation would ultimately be made by the governing country.

On the other hand, Bitcoin is inherently decentralized. It operates without a central authority or CEO and instead functions as a global network of computers, each running the Bitcoin software. This means decisions about Bitcoin are made collectively, and the network itself possesses no single point of failure. Bitcoin's decentralization not only fosters a more democratic form of money but also bolsters network resilience compared to its centralized alternative.

In summary, Bitcoin's decentralized nature allows it to transcend national boundaries, establishing itself as a global and borderless currency. This contrasts with CBDCs, which are inherently tied to national governments and central banks.

Monetary Policy

Monetary policy, which guides the management of a currency's supply and interest rates, plays a pivotal role in the economy. With CBDCs, the principles of monetary policy would likely remain consistent with the current model. Each country's central bank would continue to decide its respective monetary policies, but with the introduction of a CBDC, central banks gain a significant advantage.

The digital nature of a CBDC provides central banks with enhanced control and real-time monitoring capabilities over the currency's circulation and financial transactions within the economy. Central banks could fine-tune monetary policy more precisely and at a faster pace, reducing operational costs and facilitating tools like negative interest rates.

While this benefits central banks, its impact on individuals remains uncertain. Negative interest rates could potentially discourage individuals from saving. Additionally, concerns surrounding centralization of power and the potential misuse of such power should not be underestimated.

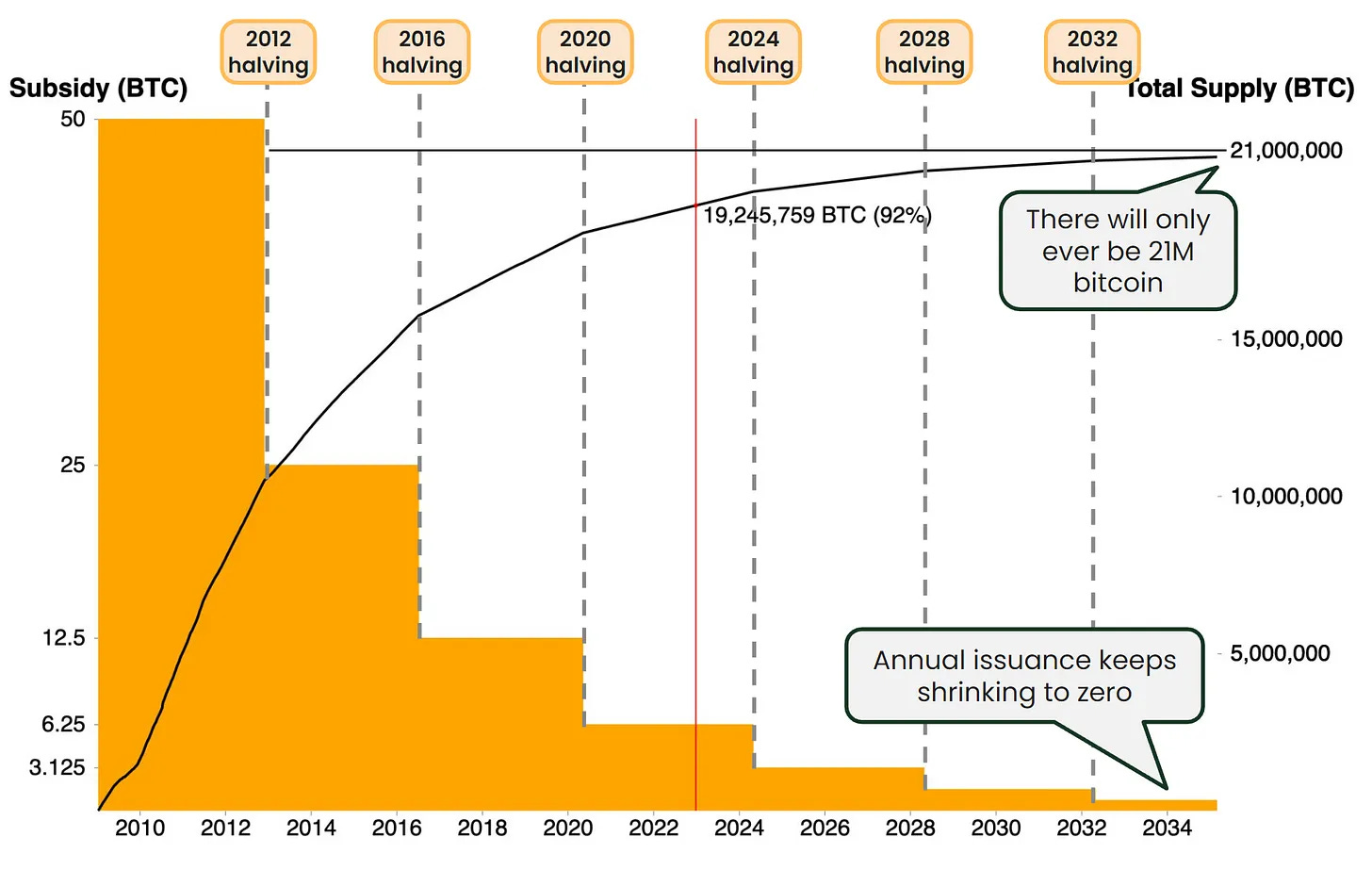

Bitcoin operates under a distinct and transparent monetary policy. The protocol is hard-coded to create a set number of new bitcoins every 10 minutes through a process known as mining.

Every four years, the amount of Bitcoin mined every 10 minutes is cut in half in an event known as the halving. This process will continue until the last of the 21 million bitcoins is mined in 2140.

Source: Jesse Myers' Bitcoin's Full Potential Valuation'

The beauty of Bitcoin's monetary policy lies in its transparency—users know its past, present, and future supply dynamics. This clarity empowers individuals to plan for the long term, make sound financial decisions, and shield their money against sudden devaluations.

Permissioned vs Permissionless

The distinction between permissioned and permissionless monetary systems plays a vital role in accessibility and inclusivity. CBDCs would introduce an increasingly permissioned monetary system, a striking departure from Bitcoin's open nature. Access to a CBDC would likely involve a registration process that requires individuals to divulge personal information, potentially hindering financial inclusion by limiting participation to only those willing to disclose personal data.

In stark contrast, Bitcoin stands as a permissionless form of money. Bitcoin is available and usable by anyone with an internet connection, fostering global accessibility and inclusion. A monetary system underpinned by Bitcoin would minimize exclusion and discrimination, ensuring broad participation.

Privacy

Privacy rights is a critical concern with a CBDC. While measures against illicit activities are important, excessive monitoring under the guise of these regulations could infringe on individual privacy. Maintaining the right balance of privacy is crucial because government overreach could undermine financial autonomy and raise concerns of intrusion.

Therefore, it is essential to ensure that any CBDC respects individuals' right to privacy and maintains a degree of anonymity. While this could be incorporated into the mechanics of the CBDC, a simpler solution would be to ensure continued access and usage of physical cash to its citizens.

On the other hand, Bitcoin transactions offer a higher degree of privacy than a CBDC. Bitcoin is pseudonymous by nature, meaning transactions made on the Bitcoin network are not directly tied to your identity but rather a cryptographic address serves as a custom identifier. This is similar to how email works—your email address serves as a custom identifier to receive digital mail but is not directly associated with your personal identity.

Censorship and Seizure

An inherent concern with CBDCs lies in the ease at which its issuing authority could censor and seize the money of those deemed threats or not in agreement with the system. The digital and centralized nature of CBDCs grants its issuers the ability to exclude individuals from the financial system and the authority to seize funds with the simple click of a button. These possibilities raise concerns regarding individual financial autonomy and government overreach.

For a financial system to be truly inclusive and non-discriminatory, it must resist financial censorship and seizure. Bitcoin, in this regard, stands as a robust solution. Being a bearer asset, Bitcoin can be self-custodied and exchanged with no intermediaries, rendering its transactions uncensorable. Additionally, Bitcoin can be securely stored in your mind by memorizing your private keys, making it immune to confiscation by force or other means. Together, these characteristics grant users of Bitcoin a much higher degree of financial sovereignty than a CBDC.

Looking to the Future

The evolving landscape of digital currencies presents many paths toward our shared financial future and global digital economy. Bitcoin, with its decentralization and finite supply, offers financial independence and resilience. On the other hand, CBDCs aim to introduce an increasingly centralized and permissioned economy, which raises concerns about privacy and government overreach. As the money we use continues to transform, individuals need to explore and understand the trade-offs associated with each alternative. The future of money is in your hands. By studying Bitcoin, you empower yourself to shape that future in a way that aligns with your values and financial goals.

Download Theya on the App Store.